10 things to consider during markets fall.

At times like this, it is sometimes worth reminding ourselves that it is this very uncertainty of shorter-term market outcomes that delivers investors with returns above those of placing bank deposits. This allows us to grow our purchasing power over time. In the case of equities, this uncertainty can be high as the market adjusts its view of long-term earnings and the discount rate it uses to establish market prices. If there was no uncertainty, then there would be no equity premium.

In contrast to the recent sensationalist headlines, such as the BBC’s ‘Coronavirus fears wipe £200 billion off the value of UK firms’ the never-published headline of ‘Over the past 10 years global equity markets have turned £100 into £266, so giving a bit back is perhaps to be expected’ provides some comfort to those already invested. To those who aren’t invested or have money to invest, stocks are cheaper than they were at the start of the year. Good news does not sell as well as bad news!

Is this time different?

You may be asking yourself whether this health-driven market event is different to those that have gone before. It is, but only because every market fall is driven by a different combination of events that impact on future corporate earnings. What should remain the same is your response to it: avoid panic, avoid unnecessary emotionally driven investment activity, believe in your portfolio and the power of markets and capitalism to recover in time.

When we build financial plans, we usually build in a disaster scenario: what happens if markets fall off a cliff? So chances are we have already considered for a substantial market fall, we just didn’t know when it would happen, nor what would cause it.

Here are some tips to help keep things in perspective:

10 things to consider during markets fall.

Embrace uncertainty

Embrace the uncertainty of markets – that’s what delivers you strong, long-term returns. Remember that you most likely own bonds in your portfolio too. Your portfolio won’t be down as much as the headlines.

Timescale

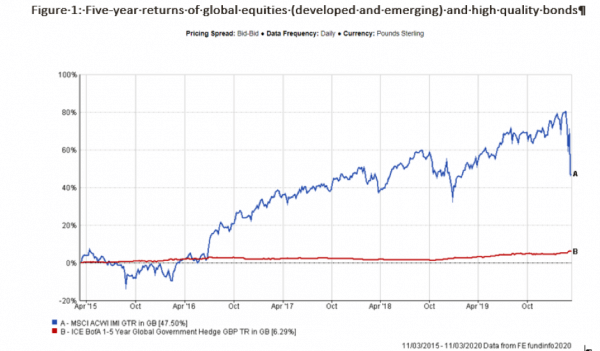

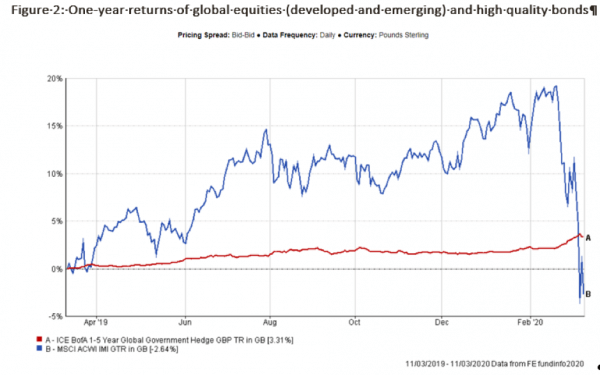

Don’t measure your portfolio’s performance from the top of the market, but over a longer and more sensible timeframe. Take a look at the charts below. Over the past five years, investors have received handsome growth. Even over the past year, equities are only a little below where they started.

Forget about it

Don’t look at your portfolio too often. Get on with more important things. Once a year is more than enough. If you are looking every day, then have a word with yourself – you are probably causing yourself unnecessary anxiety. And when consuming media, remember that good news doesn’t sell.

Market timing

Accept that you cannot time when to be in and out of markets – it is simply not possible to do it successfully and consistently. Resign yourself to the fact. People predict crashes every year and as the chart above shows, they are almost always wrong. Even a blind squirrel finds the occasional nut.

You still own the assets

If markets have fallen, remember that you still own everything you did before (the same number of shares in the same companies, and the same bonds holdings).

Investing is for the long term

Most crucially, a fall does not turn into a loss unless you sell your investments at the wrong time. If you don’t need the money, why would you sell? Falls in the markets and recoveries to previous highs are likely to sit well inside your long-term investment horizon, i.e. when you need money to do the things that are really important to you.

Diversification

Be confident that your (boring) defensive assets will come into their own, protecting your portfolio from some of equity market falls. You can see this in action in the one-year chart above. Be confident that you have many investment eggs held in different baskets.

Asset allocation & risk

The balance between your growth (equity) assets and defensive (high quality bond) assets was established between you and your adviser to make sure that you can withstand temporary falls in the value of your portfolio, both emotionally and financially. If necessary, your adviser may rebalance your portfolio to make sure that you have the right level of equities to benefit from future market rises.

Ask for help from your financial planner

We are here – at any time – to talk to you. Our job right now is to act as your behavioural coach to urge you to stay the course, to encourage fortitude, patience and discipline, at a time when that can feel very uncomfortable and counter-intuitive.

Look out for others

You may well have friends and family that are feeling just as bad as you, and maybe worse if they don’t have a financial planner – feel free to share these messages with them. We don’t have a crystal ball – nobody does – but history has sown that short-term emotional decision usually do a lot more harm than good.

I understand that you are probably feeling very uncomfortable right now, and I want you to know that I know how you are feeling – I really do. Not only do I have my own pension and savings invested in exactly the same way that you do, but I also feel very much the responsibility of helping our firm look after hundreds of millions of pounds of your money and other clients.

Stay strong, and don’t suffer in silence – we’re in this together, and the Navigator team and I are here to help.

Please note that past performance is not a guide to the future, the value of an investment and the income from it could go down as well as up. You may not get back what you invest.

Data: MSCI ACWI IMI Index 1/2010 to 2/2020. Source: Morningstar Direct © All rights reserved.